Key Insights

This section summarises the main economic findings from the dashboard. It highlights insights across GDP, trade, inflation, employment, remittances, and fiscal policy in the period leading up to and throughout 2023.

GDP Trends

Zimbabwe’s GDP figures were reported in constant US dollars. Between 2019 and 2023, the economy grew at an average annual rate of 1.63%.

There were two years of contraction in 2019 and 2020, followed by a recovery in 2021 and 2022.

The strongest growth was recorded between 2020 and 2021, reaching 8%.

Trade Balance and Export Partners

During the same period, Zimbabwe recorded a negative trade balance of –$1.87 billion USD,

meaning the country imported nearly $2 billion more than it exported.

Most of Zimbabwe’s exports went to Sub-Saharan Africa, with South Africa being the top destination.

The second largest export destination was Western Asia, specifically the United Arab Emirates.

I also included a detailed breakdown of imports and exports by HS code to show which goods were traded.

Inflation and Monetary Policy

Inflation in 2023 was severe. In June, the year-on-year inflation rate stood at 175.75%,

while the rate for food and non-alcoholic beverages alone was a staggering 255.6%.

Month-on-month inflation for June reached 74.46%, reflecting ongoing price instability.

The five categories with the highest year-on-year inflation in June were:

- Communication

- Food and non-alcoholic beverages

- Housing, water, electricity, gas, and other fuels

- Recreation and culture

- Transport

Monetary policy data also showed exponential growth in the money supply (M2),

pointing to increased liquidity in the economy and a likely contributor to inflationary pressure.

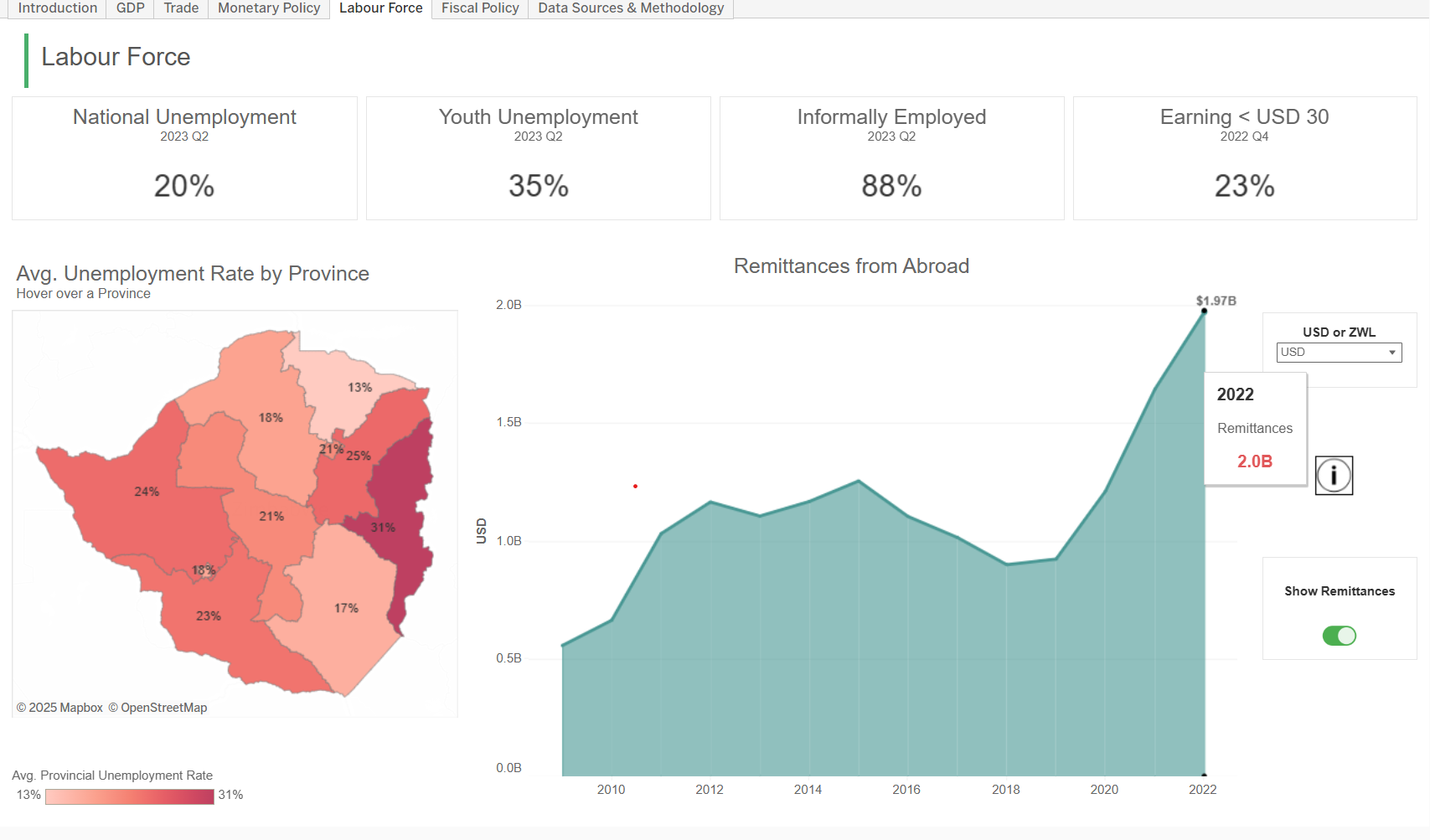

Labour Market Conditions

Labour force data revealed several structural challenges. In the second quarter of 2023,

national unemployment stood at 20%, with youth unemployment reaching 35%.

ZIMSTAT also reported that 88% of the labour force was informally employed—highlighting the dominance of informal work in Zimbabwe’s economy.

In the fourth quarter of 2022, 23% of workers were earning less than $30 USD per month.

Remittances

Remittances from abroad played a critical role in supporting Zimbabwean households.

From 2018 to 2022, total remittance inflows grew from $0.9 billion to $1.97 billion USD,

showing just how vital the diaspora has become in stabilising incomes.

Fiscal Policy and Debt

On the fiscal side, government spending and borrowing remained under pressure.

By the end of 2021, Zimbabwe’s public debt-to-GDP ratio was 85%,

indicating that the country owed debt equivalent to more than four-fifths of its entire annual economic output.

While this figure includes both domestic and external debt, it raises concerns about fiscal sustainability—particularly in a context of slow growth, high inflation, and currency instability.